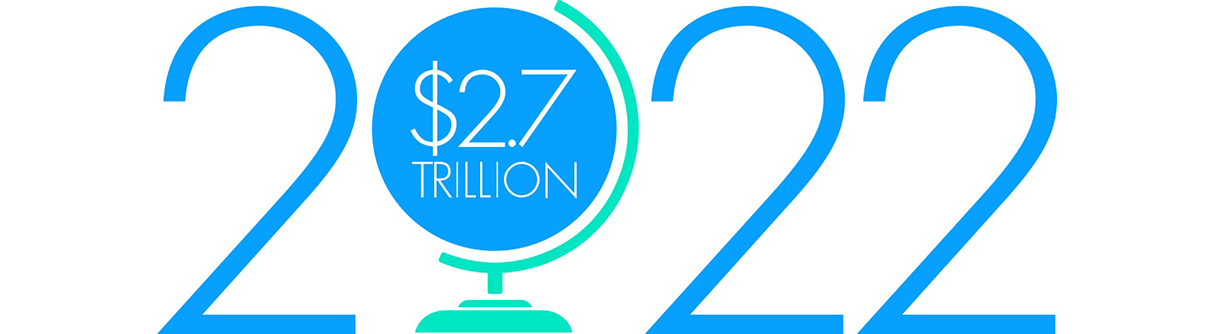

Are fuel stations dying? It’s a strange question to ask of a market that is expected to reach $2.7 trillion in revenue globally by 2022.1 But with the rise of alternative fuel sources, ride sharing, electric vehicles and the impact of changing consumer behaviors and evolving regulations, the question is not so outlandish.

To explore what the fuel station will look like in 2025—and whether it will one day go the way of drive-in movie theaters and public telephone booths—we talked with Publicis Sapient energy and commodity experts in several geographies.

Iyad Ghanem, director, offered a view of the market in France. Over the past decade, the country has seen more than half of its fuel stations close, and retailers now own as many stations as the supermajors do. Ghanem’s perspective? Fuel stations aren’t dying. But they are on the road to being very different.

Interview has been edited for style and clarity.