The U.K.’s Consumer Duty regulation took effect earlier this summer, requiring banks to maximize their efforts to put their customers’ interests at the center of their practices. Customer segmentation will play a critical role in helping banks understand their customers' needs and preferences and tailor their marketing messages and product offerings accordingly. Many banks, however, still use traditional 1D or 2D segmentation maps and visualizations, which do not fully reflect customers’ complex behaviors and needs.

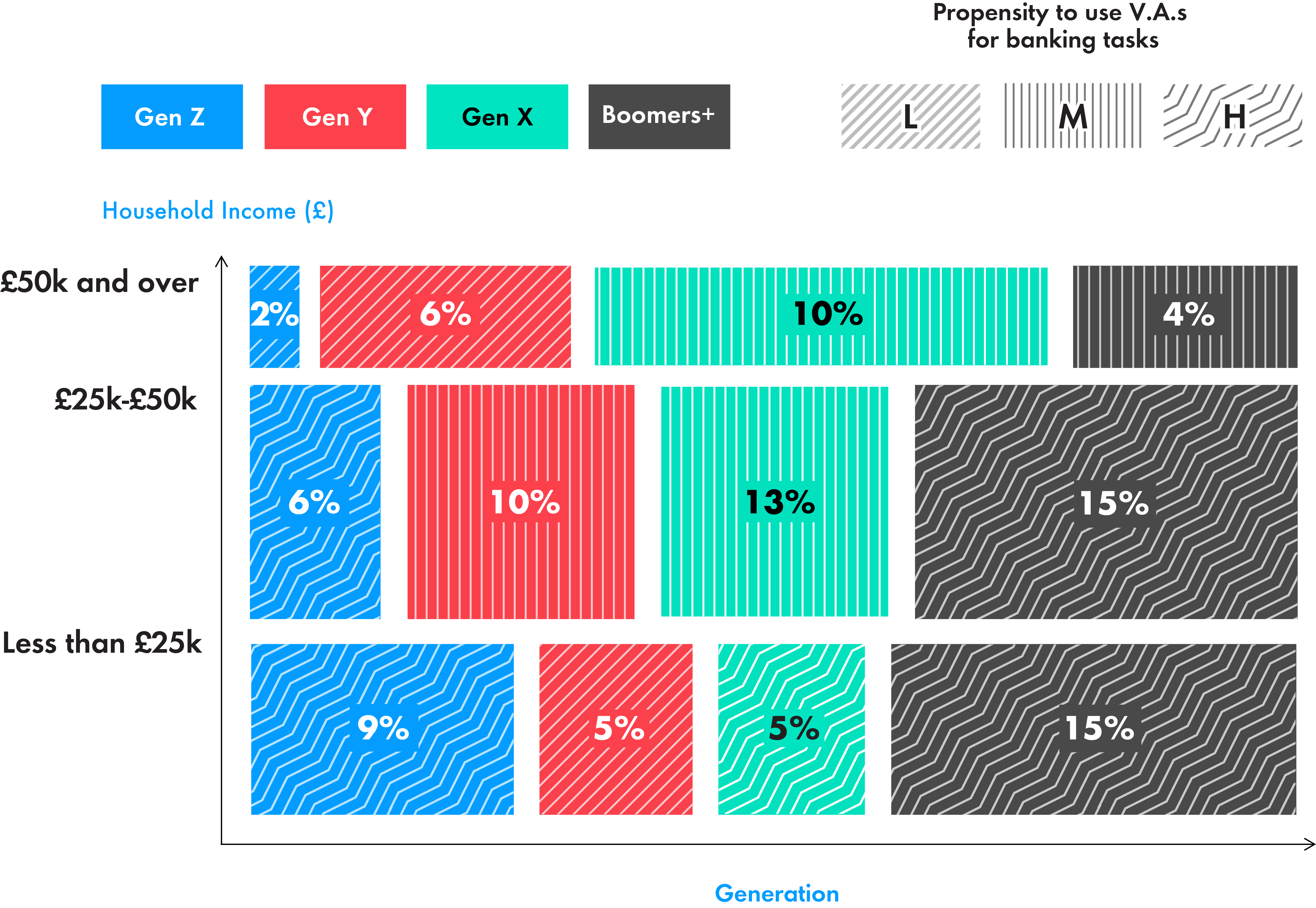

We examine various segmentation visualization techniques as well as their limitations, exploring the importance of incorporating psychographic data and introducing 3D maps as a more reliable method of customer segmentation. This article is aimed at equipping professionals with the knowledge to take the first steps in better understanding their customers.

What is customer segmentation?

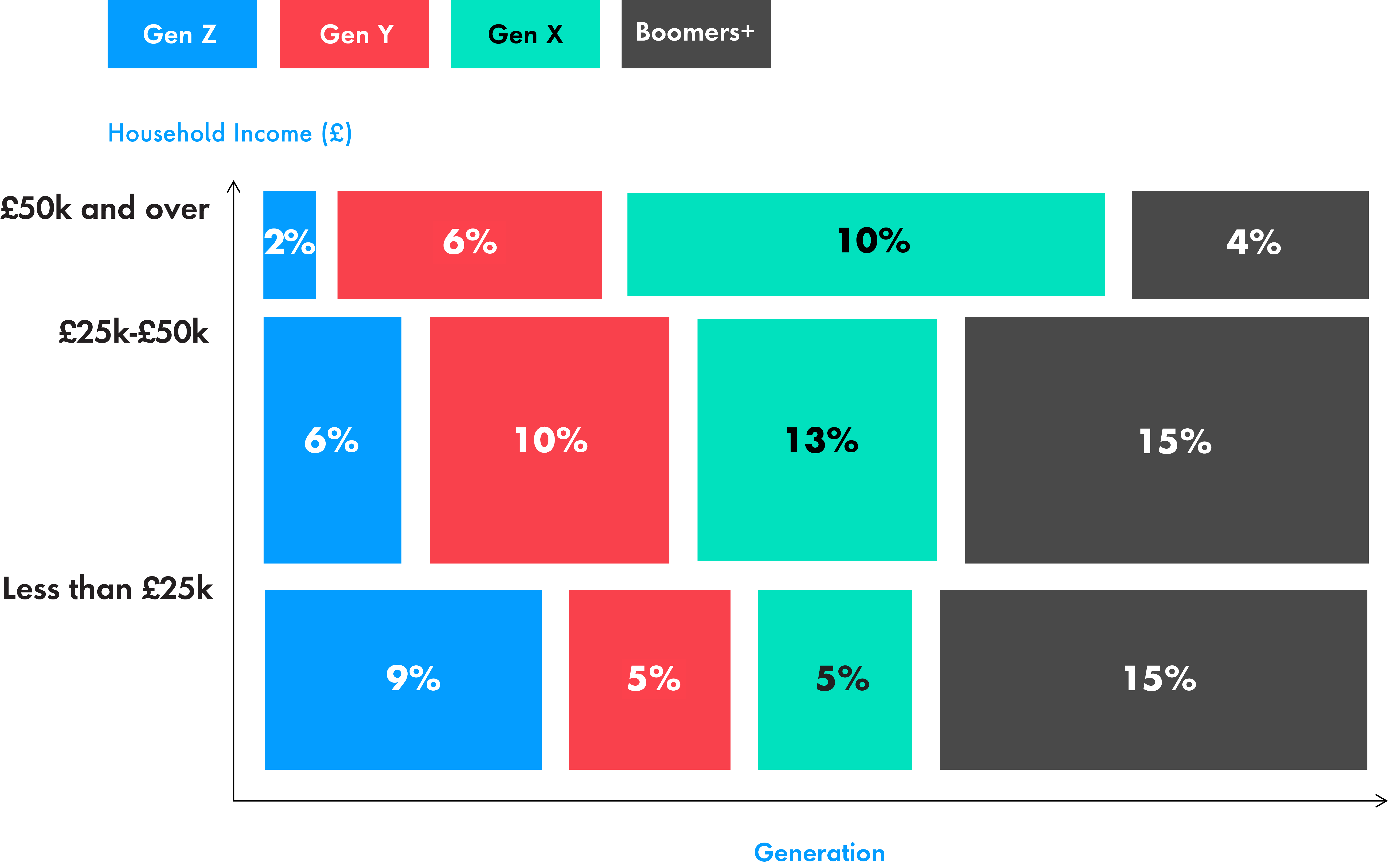

Customer segmentation is the process of dividing a business’s market into subgroups of consumers based on specific behaviors or characteristics. While traditional 1D or 2D segmentation maps, which rely on demographics and basic data, have been widely used by banks, they fall short of capturing the complexity of customer needs and behaviors.

Enhanced segmentation makes it possible for financial institutions to deliver tailored, personalized offerings to their customers and comply with Consumer Duty. Some are even beginning to think bigger and are incorporating AI and ML in their efforts.

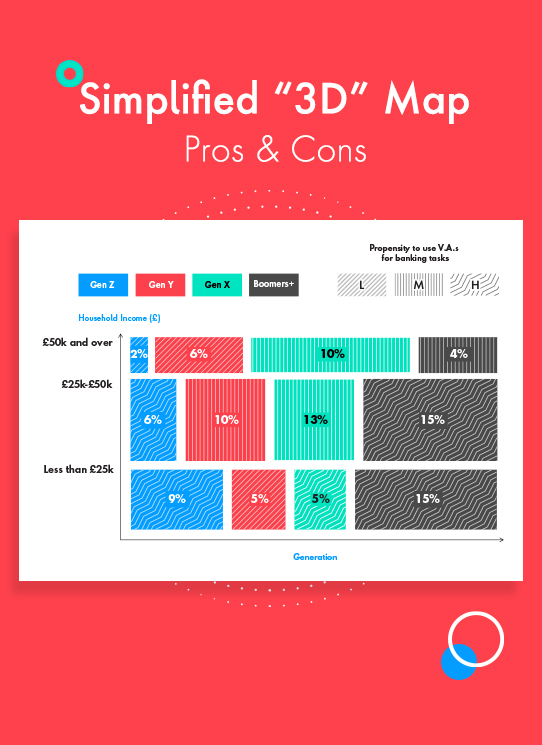

Types of customer segmentation: what banks do today

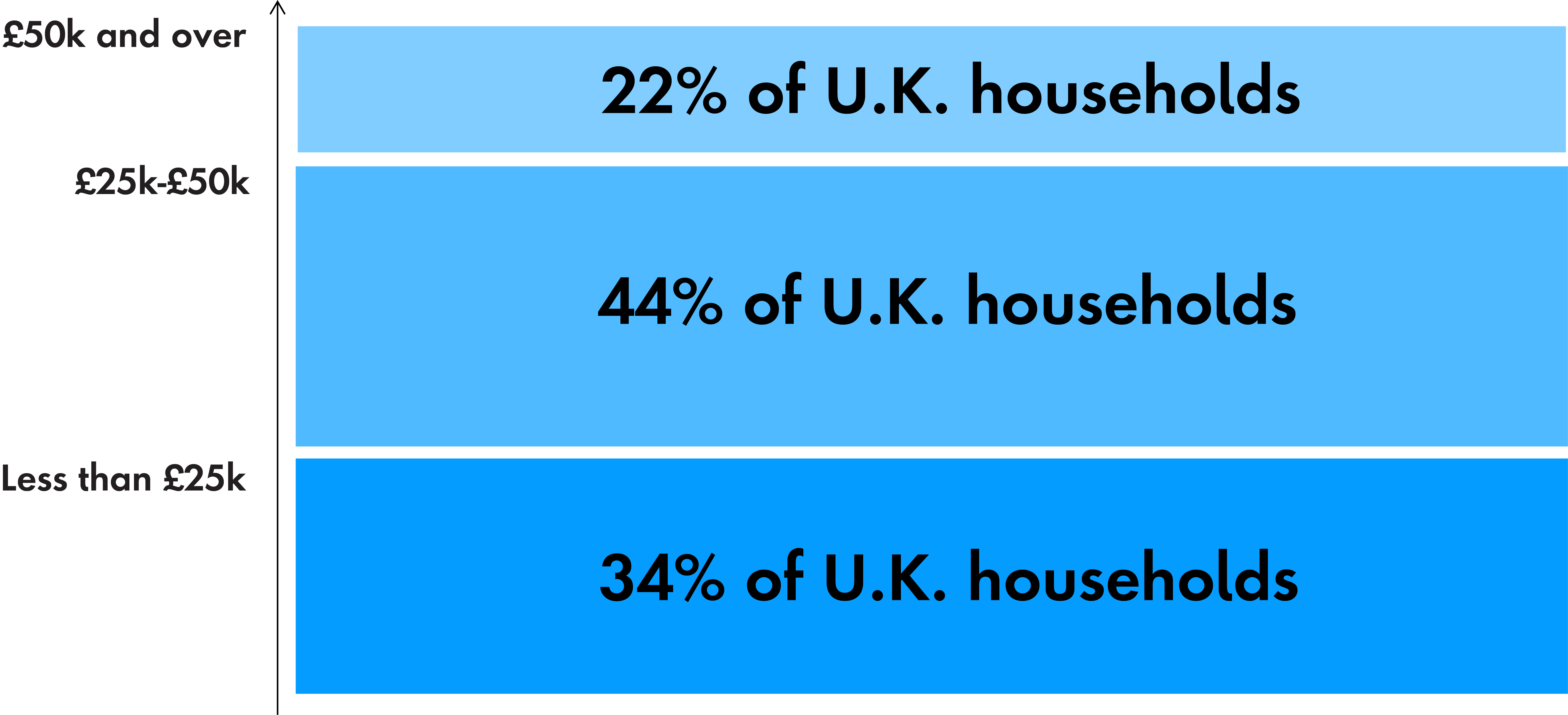

Today, some banks’ departments still rely on 1D segmentation visualizations (or maps) that primarily focus on income or location. Such maps are one of the simplest methods of customer segmentation and are useful for targeting broad customer groups but fail to provide a detailed view of customer behavior and preferences, which is at the core of the regulator’s expectations.