Many financial services companies talk floridly about being customer centric. Customers have surely never had it better.

As advertising guru Bill Bernbach once said, “A principle isn’t a principle until it costs you something.” When talking about the principle of customer centricity, many companies focus on the intersection of what’s good for the company and what’s good for the customer. Customer centricity as long as it makes the business money in the short term. Customer centricity with an asterisk.

One of the reasons companies cannot translate customer needs and wants into products and experiences is because they don’t understand the “why.” Digitalization has resulted in companies gaining access to accurate data in a timely fashion. Mobile apps, ecommerce platforms and websites of all varieties generate a large amount of data which is turned into dashboards, reports, insights and ultimately some form of data-driven decision making. Digital is data after all.

However, those 1s and 0s rarely provide an insight into the motivation of a customer. Various studies suggest that over 70% of interpersonal communication is non-verbal1. Good luck capturing that information from a mobile or web application. The problem with most digital analytics is not a lack of data, but the means to analyze that data to generate actionable insight beyond the blindingly obvious.

In a Harvard Business Review article2, leadership luminary Thomas Davenport reported that less than 1% of a company’s unstructured data gets analyzed. If you combine that figure with the broadly published and generally accepted heuristic that 80% of a company’s data is unstructured, there is a sizeable blind spot in customer understanding.

Every company is sitting on a veritable gold mine of insight in the form of customer service interactions, in-bound customer contacts, field engineer reports, key account manager conversations, contracts, customer satisfaction surveys (the long answers that nobody reads) and product reviews. This data is freely offered and when it comes to customer reviews, publicly available.

Fortunately, advances in machine learning, particularly in the field of natural language processing (NLP), have made the process of mining unstructured data for gold significantly more accessible.

To prove the point, we analysed over 100,000 customer banking reviews from publicly available sources to rate and compare customer experience across Tier 1 and Tier 2 Banks, as well as Neobanks, within the UK using our Customer Experience Growth Index. The world of customer reviews can easily be gamed. There is a strong positive correlation between the number of reviews a bank has and the score (generally out of five stars) it achieves. This is largely due to some banks engaging in managing their customer service score with a customer review company. So, an analysis of customer review scores only yields limited insight. Almost all banking mobile apps in the UK achieve 4.9 or 4.8 scores on the Apple Store, making the scores practically meaningless. Analysis loves variance. The variance can be found in the verbatim review comments rather than the star rating.

An analysis of language comparing good and bad reviews reveals the insights you would expect. People use positive words in five-star reviews and negative terms in one-star reviews. Instead, we compared the language used in five-star reviews only, and compared the differences between banks, to isolate the things consumers like about their provider when they are happy with their bank.

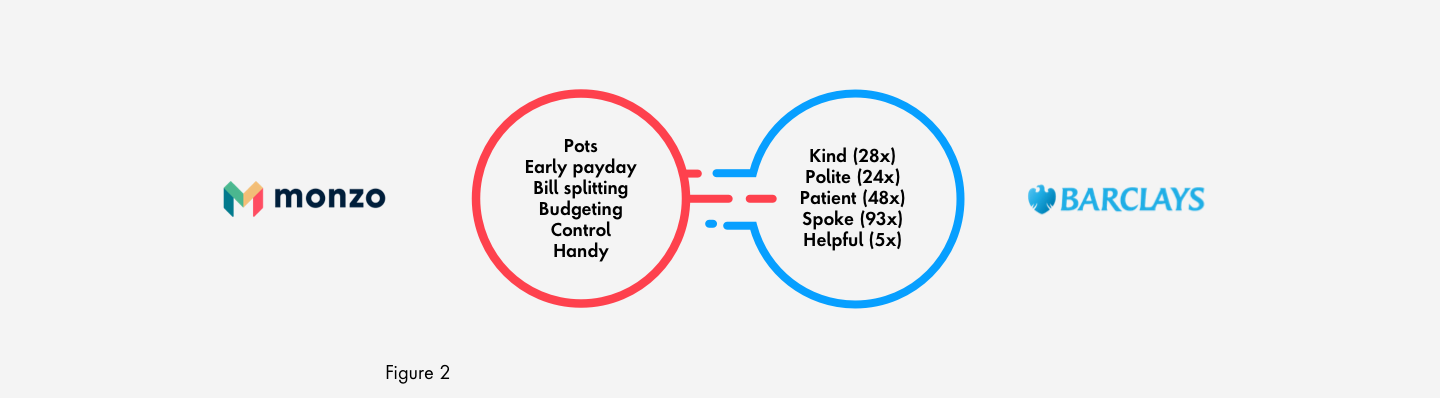

Looking at the UK banking sector, there is a clear divide between challenger banks and their established high-street rivals. When challenger banks are compared head-to-head what we see is a battle over features.

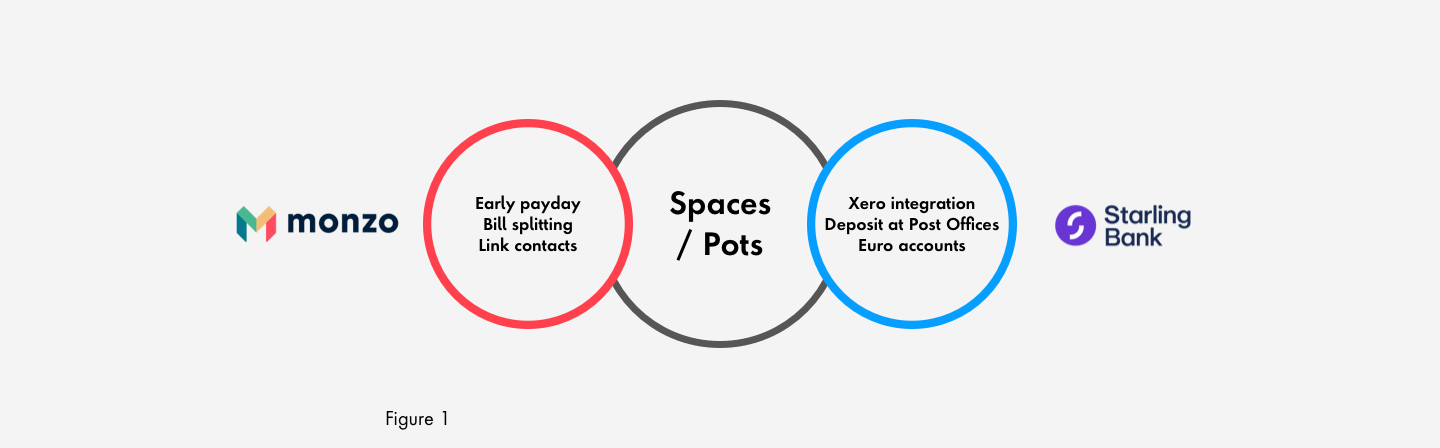

Figure 1 is a Venn diagram of topics that appear in Monzo and Starling Bank five-star reviews. Both challenger banks have a feature, Pots for Monzo and Spaces for Starling, which allow the customer to divide their current account up into separate pools of money to either save, pay bills or fund their social life. Monzo five-star reviews predominantly focus on key features of bill splitting (being able to pay a bill between friends), easy upload of phone contacts as payees and being able to access your salary at 4pm the day before its paid in. All key features that Monzo has innovatively brought to the market. Starling on the other hand has reviews that cover its own feature set, the ability to integrate with Xero accounting software, to pay cash into post offices in the UK and to be able to set up accounts in different currencies.