What issue can we solve for you?

Type in your prompt above or try one of these suggestions

Suggested Prompt

Insights

How Blockchain Could Power Digital Currency in U.S.

How Blockchain Could Power Digital Currency in U.S.

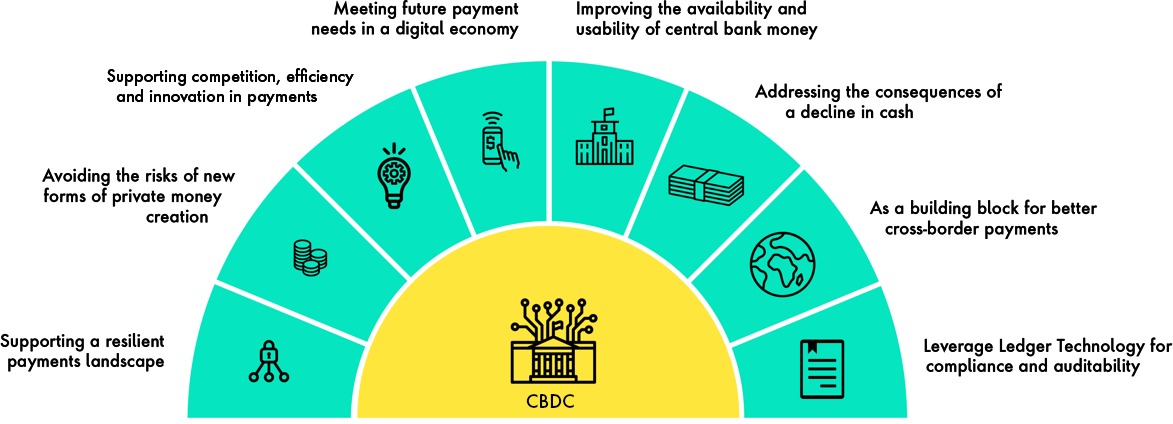

Unlike other leading economies, the United States’ government does not have direct money-distribution mechanisms in place, which hinders efforts to help people who don’t have access to banking services during good times and grueling during crises. The majority of the Central Banks across the world responded with an indication of active involvement with some version of G2C (Government to Citizen) or CBDC (Central Bank Digital Currency), as per the latest Bank of International Settlements survey.

The lack of direct G2C (i.e., public) payment systems stymied the government’s response to the COVID-19 pandemic. For example, without a digitized fiscal payments system, the U.S. Treasury and Small Business Administration could not send stimulus payments to citizens directly. Instead, this assistance was routed through intermediaries – costing billions in taxpayer dollars and creating unnecessary delays.

In reaction to this dilemma, bipartisan groups of lawmakers in the House and Senate proposed bills that would establish digital dollars and allow citizens to set up checking accounts directly with the Federal Reserve. But the central bank’s current technological infrastructure is ill-equipped to handle the distribution and management of a digital fiat currency.

Publicis Sapient technologists Suresh Kandula and Gaurav Verma have been working on conceptual solutions related to cryptocurrencies that would be applicable for Financial Services for years, including secured lending, secured loans, decentralized secure chat, etc. They are developing a proof of concept (POC) that would enable the use of digital dollars by fiscal policy stewards (intermediaries, banks, and other governmental organizations) involved in a nation’s policy, including government agencies like the U.S. Treasury and industry consortiums like the Depository Trust & Clearing Corporation (DTCC).

“The Federal Reserve and other central banks haven’t put any real effort towards digital currency. But the current pandemic has pushed us in the direction of a G2C payment ecosystem,” Verma said. “We can clearly see the evidence in early drafts for COVID-19 stimulus packages. ‘Digital dollar’ and “digital dollar wallet’ were mentioned multiple times.”

Unlocking blockchain and other distributed ledger technologies is the key to mobilizing nationwide digital currencies. Transactions would be easy, safe and efficient.

“This is really about making transactions effective, even more than we’ve been seeing in Asia, Europe and other places. That’s based on foundational platforms such as distributed ledger, centralized ledger, blockchain and cryptocurrency,” Kandula said.

Unlocking blockchain and other distributed ledger technologies is the key to mobilizing nationwide digital currencies. Transactions would be easy, safe and efficient.

Connect the network

Blockchain is a decentralized database of transactions distributed across a network of computer systems. In this case, the “chain” is the system that links the “blocks” or digital information. Each block of information is recorded with a unique alphanumeric signature, called a hash, which can be accessed throughout the network.

Silicon Valley has long appreciated the utility and promise of blockchain’s ability to circumvent traditional gatekeepers of data. Cryptography algorithms verify and broadcast different transactions so companies can track their entire histories without paying or relying upon middlemen.

Once a future-facing bill embracing the digital dollar is passed, organizations will invest heavily in the concept to make sure they do not fall behind. Every organization that wants to be part of the digital dollar program would need to have the blockchain.

Blockchain is particularly intriguing to newer companies because of the infrastructure’s widespread availability. There would be an open-source network of digital dollar participants – utterly transforming how people handle personal finance.

Verma said a central bank digital currency (CBDC) could connect the unbanked population and the government in a myriad of ways that advances productivity and fiscal well-being.

Provide digital wallets

Citizens would be able to apply for a digital wallet that’s connected to their personally Identifiable Information (PII). Any approved institution or person – the government, a company, a friend, etc. – would be able to deposit money directly into the cryptographically secure wallet.

“The wallet would be tied to your social security number or another national ID,” Kandula said. “That way you can access and send money without going through all these banks and apps that charge a lot of commissions. They don’t have control over your identity because they are private organizations.”

This would apply to anyone who currently has a G2C relationship and include all unbanked citizens, so it would be more inclusive than what’s currently available.

In addition to spurring economic growth, central banks would benefit from cutting the costs of printing and distributing new money to the point that “seigniorage” becomes virtually nonexistent. Seigniorage is the difference between the value of a piece of currency, such as bank notes, and the cost the produce it.

“This is a very unique opportunity,” Verma said.

“This is a unique opportunity.”

Gaurav Verma , Senior Director – FinTech Practice at Publicis Sapient

Make it personal

The digital wallet would essentially use the same technologies that enable citizens to trade stocks amongst themselves or move them from one bank to another.

“Now everybody can send money to each other because they're all part of the network, and then they know when money is being transferred from organization to organization, or person to person, citizen to citizen, or government to citizen. It’s no longer about physical cash and bank accounts,” Kandula said. “This is going to make it more approachable for unbanked and millennials.”

Over time, citizens will be able to use their digital wallets for trips to the store or online purchases in place of credit or debit cards.

“It’s really about giving the customer the power,” Kandula said. “Wallet means you are controlling it just like password protection. You decide who you're sending it to, and then if you are receiving, you could say whether you want it or not.”

Embrace the future

The extraordinary volatility after the onset of COVID-19 exposed shortcomings and blind spots in the financial services industry.

Financial institutions have been capitalizing on cutting-edge technologies to offer new services and products. But the approaching digitization of fiat monies, securities and mortgages will propel business process automation forward and increase efficiencies for transactions and trades. Institutions are looking to digitize their respective currencies, securities (stocks, bonds) and other contracts.

This would revolutionize the world of finance and regulation. Nicolas Xuan’s analysis highlights the financial stability improvement a CBDC can bring without degrading credit availability in the long term by removing certain market subsidies that promote poor risk practices and improper pricing.