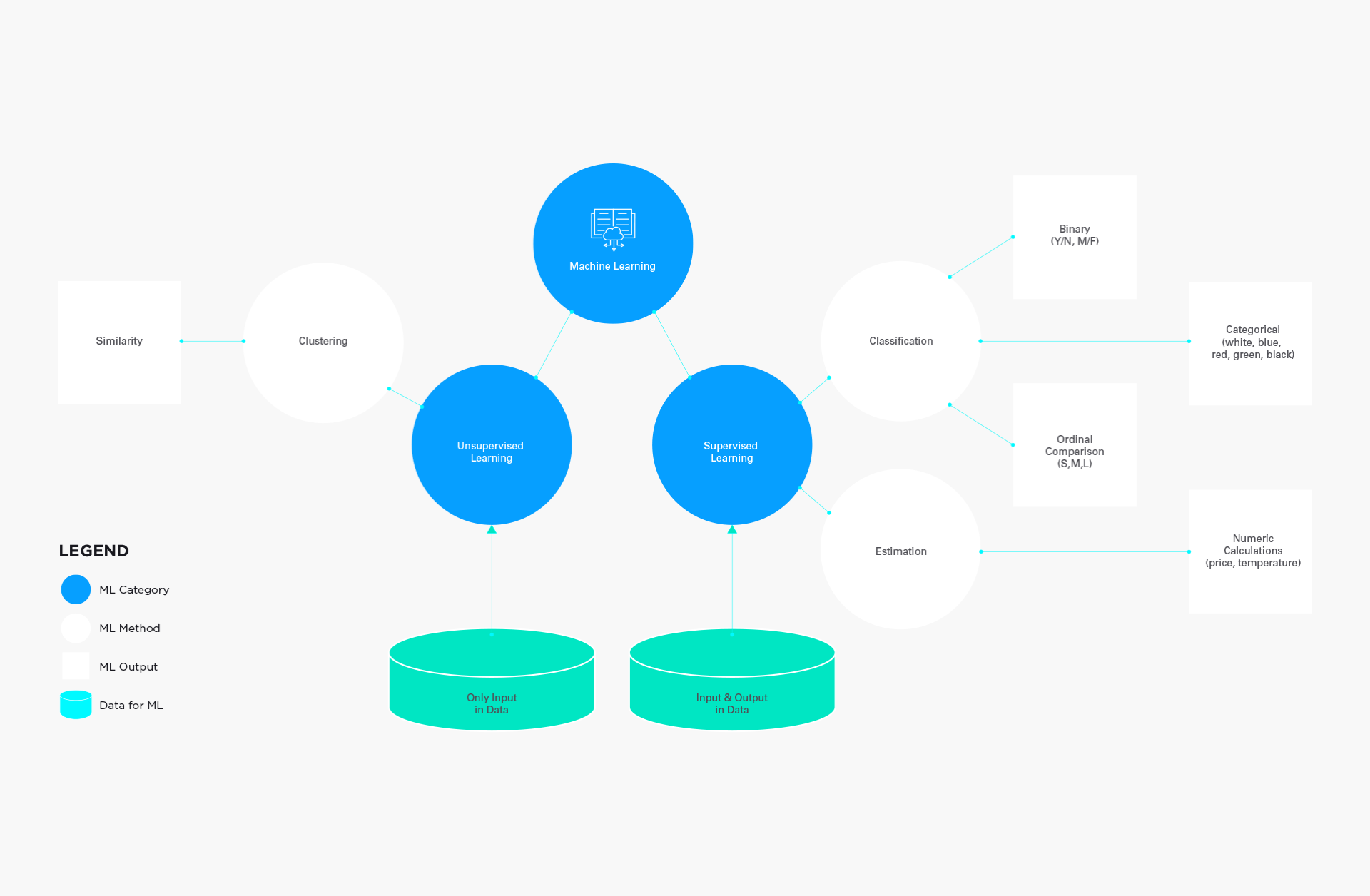

Deliver business performance breakthroughs with machine learning

As emerging technologies in AI, machine learning and data science mature, leading business executives find ways to operationalize it.

What's hard for people is easy for machines

If you’ve ever watched one of the many popular television shows about law enforcement, business or medicine you’ve seen the scenario where an army of young associates pore through boxes of files to find that piece of insight that might pave the way toward resolving a life-threatening situation.1

Maybe they’re attorneys searching for a legal argument for a high stakes trial or young doctors trying to predict how a patient will react to a treatment or a bunch of traders eager to know which supplier stocks will go up when Apple introduces its next iPad.

Smart machines offer an attractive business case

The people searching for the story in the data are highly educated, well-paid and often work all night, days and weeks to find evidence or patterns of insight that can be used to solve a problem. Even when the scenarios are conducted online, these smart associates often need to digest each file as they search for the story.2 And, as humans become exhausted, they make mistakes or overlook a detail. Enter smart machines, who will work 24/7, never tire, and will never demand overtime.

Smart machines are an effective substitute for what humans find unfathomable: digesting enormous volumes of data, taking into consideration each and every fact the data represents. Business people excel where smart machines do not: making decisions from the facts, context and background. Elbert Hubbard sums it up: “One machine can do the work of fifty ordinary men, yet no machine can do the work of one extraordinary man.” Put another way, “What’s hard for people is easy for machines; what’s hard for machines is easy for people.”3 For example, equipped with enough learning data, a smart machine can perform sales analysis on millions of products, but it cannot judge whether a decision to offer a higher price for loyal customers is ethical. Hence, these initiatives require the organization’s combined experience and skills with new smart machine capabilities.