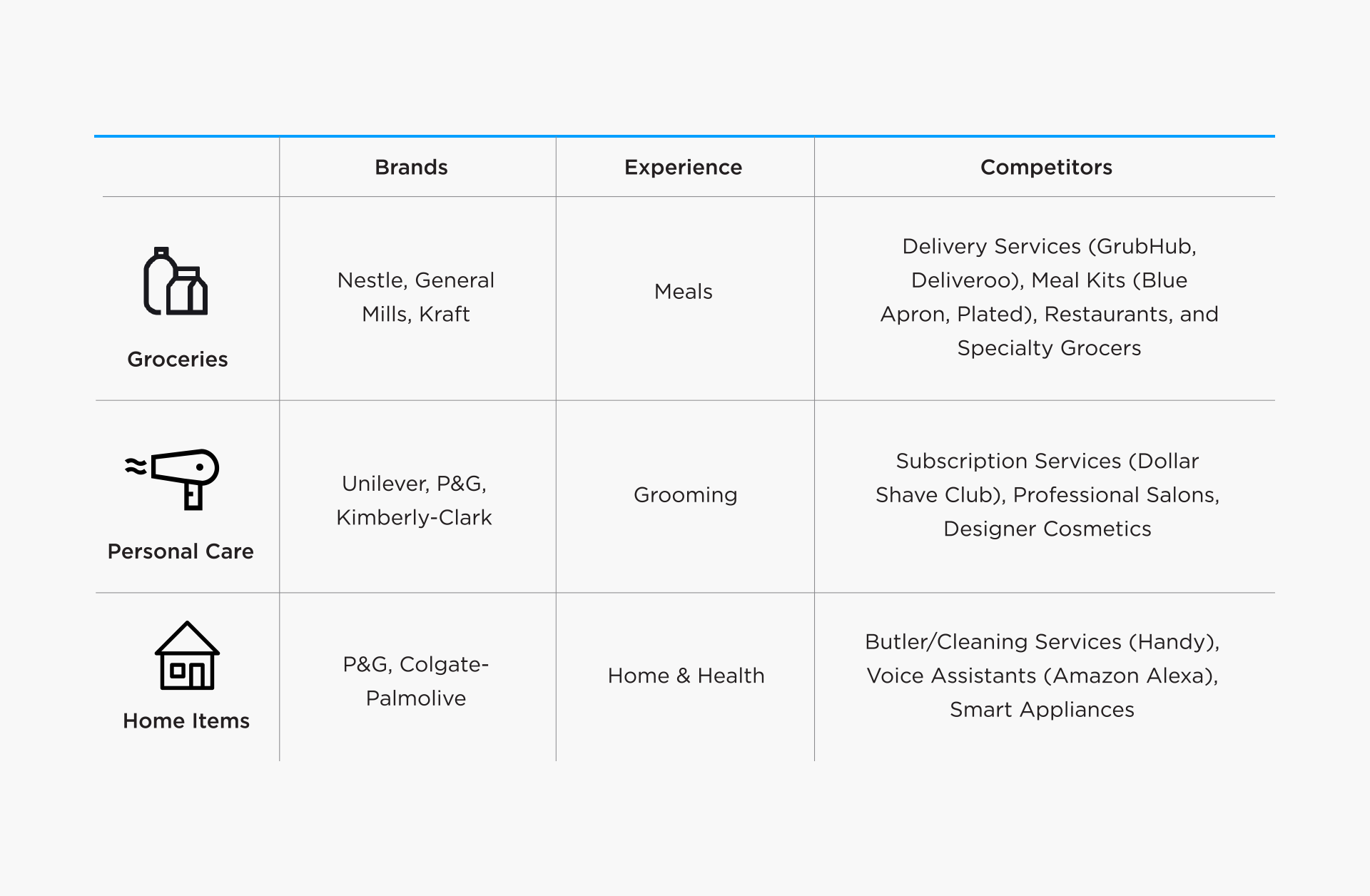

These are questions that brands ask with great urgency. Organizations must consider the ramifications of operating in a landscape that is being massively disrupted by a new competitor group that we call experience providers, disruptors that organize their business models around providing robust consumer experiences—as opposed to product manufacturing and distribution.

The new experience providers take various forms: voice assistants like Amazon’s Alexa that revolutionize how and when people shop for groceries and household products, smart appliances like Whirlpool’s new Amazon Dash–integrated washing machine that automates the purchase of common household goods, and product platforms like Blue Apron or Dollar Shave Club that prompt consumers to rethink everything from meal prep to grooming. In other words, for traditional brands, the product is the product. For this new breed of company, the experience is the product.

Why is this significant? Because in creating new ways of interacting with consumers, experience providers are building valuable, ongoing relationships with their customers. In many cases, they are replacing the role that traditional consumer products companies once played in customers’ lives. Slowly, these experience providers are assuming real purchasing power as voice assistants decide what milk to buy, and meal services choose which ingredients to source. At the same time, these brands are eliminating many valuable opportunities for in-store product discovery by limiting the customers’ trips to a retail location. After all, why drive to Walmart to buy groceries when Amazon delivers them to your door?

As consumers continue to become more comfortable with in-home technology, and brands deliver on the promise of simplicity and convenience, it is the experience provider that could eventually come to own the customer relationship by deciding which brands to buy, when to order them, and how to deliver them. And, increasingly, the brands that they recommend are their own. According to research from the Private Label Manufacturers Association, retailers’ own brands (private labels) accounted for $150B in sales in 2016 alone, and that number is growing fast.³ With this in mind, brands are faced with a real choice: become an experience brand... or be relegated to a mere product provider to retailers’ own brands.