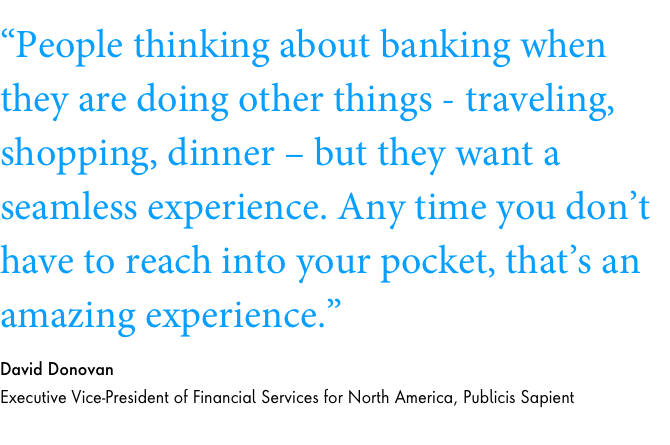

The nature of banking is changing. Embedded finance is turning every app, retailer and business into a bank. Today’s consumer demands flexibility in how and where they engage with financial services to get what they want. “Banks that take advantage of this shift will outpace their customers and seize a new generation of customers across a multitude of channels. Banks that fail to adapt risk extinction,” said David Donovan, executive vice-president of financial services for North America at Publicis Sapient.

We were proud both to sponsor and speak at Tearsheet’s recent Embedded Conference, where a common thread ran through the sessions: that banking will soon be woven inextricably into consumers’ relationships with the brands they love.

As Donovan emphasized in a recent interview with Tearsheet, embedded finance provides opportunities for banks to integrate with other brands to offer new products and services to their customers.

Here are five key takeaways from the conference.

Takeaway 1

Banks are facing big strategic decisions

Covid-19 has intensified the tough economic conditions that squeeze banks’ profitability, noted David Murphy, managing partner, financial services EMEA and APAC at Publicis Sapient. But it has also accelerated technology shifts – digitization is turning banks into technology companies and their banking services are becoming largely commoditized.

They must respond by speeding up their transformation programs and rethinking distribution channels and the way they engage customers.

This is unfamiliar territory, and many banks are unprepared. How should they respond? The key strategic question is whether to become “financial plumbing”, leveraging their balance sheets but plugging into other marketplaces via tie-ups such as Amazon/Goldman Sachs or Google/Citi, or to “make the market” by expanding into non-traditional services.

This embedded finance model is becoming an integral part of many banks’ plans, driven by their need to revitalize growth by rethinking the way they engage customers.

But to succeed, banks need to be hyper-efficient, utilize customer data much more effectively and be more innovative and flexible in their product development and delivery. This means their senior executives must have an intimate understanding of the platform model and a strong commitment to speed up the transformation.

Takeaway 2

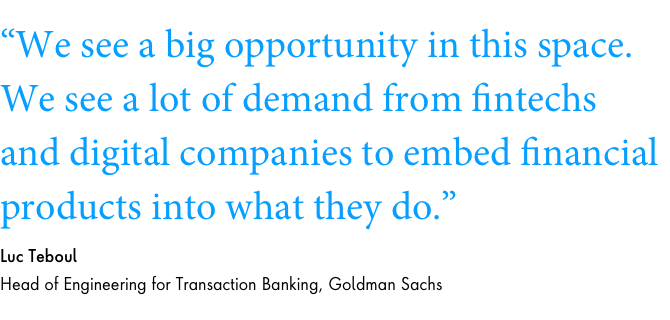

Why Goldman Sachs moved into Banking-as-a-Service

Goldman Sachs is pushing into the Banking-as-a-Service market with its cloud-native transaction banking platform, Luc Teboul, head of engineering for transaction banking, told the Behind the Build session. The platform, which Publicis Sapient helped to create, was originally intended to deliver digital solutions to the bank’s treasury clients. But now Goldman has much bigger plans for it.

Goldman has co-designed the platform with its clients and will integrate it seamlessly into their business. “We have evolved our platform based on the solution that our partners wanted,” said Teboul.

The platform is available in the US currently, but Goldman is working towards launches in Europe and Asia, and over the coming year will expand its capabilities to include a multi-currency offering.